Good evening investors!

This week I am making some small tweaks to this newsletter with the goal of making it more helpful for you.

First, you'll notice the title which starts with "[+2.4%]." This is the weekly percentage change in the S&P 500. That way, even if you don't have time to read the latest newsletter, you'll at least have a sense of whether the market is up or down lately.

Second, I've added a "Mastery" blurb at the end of each section. My goal here is to give you the "so what" of each update. Instead of simply reporting the news, I want to make sure you the reader have a clear understanding of what this means for you and your portfolio.

Let's get into it.

-Brian

In Today's Issue:

🥇 Stocks Continue Their Record Run

🥈 Corporations Are Making So Much Money

🥉 The Federal Reserve is Playing Hard to Get

Markets

Tariff Tantrums & Record Runs

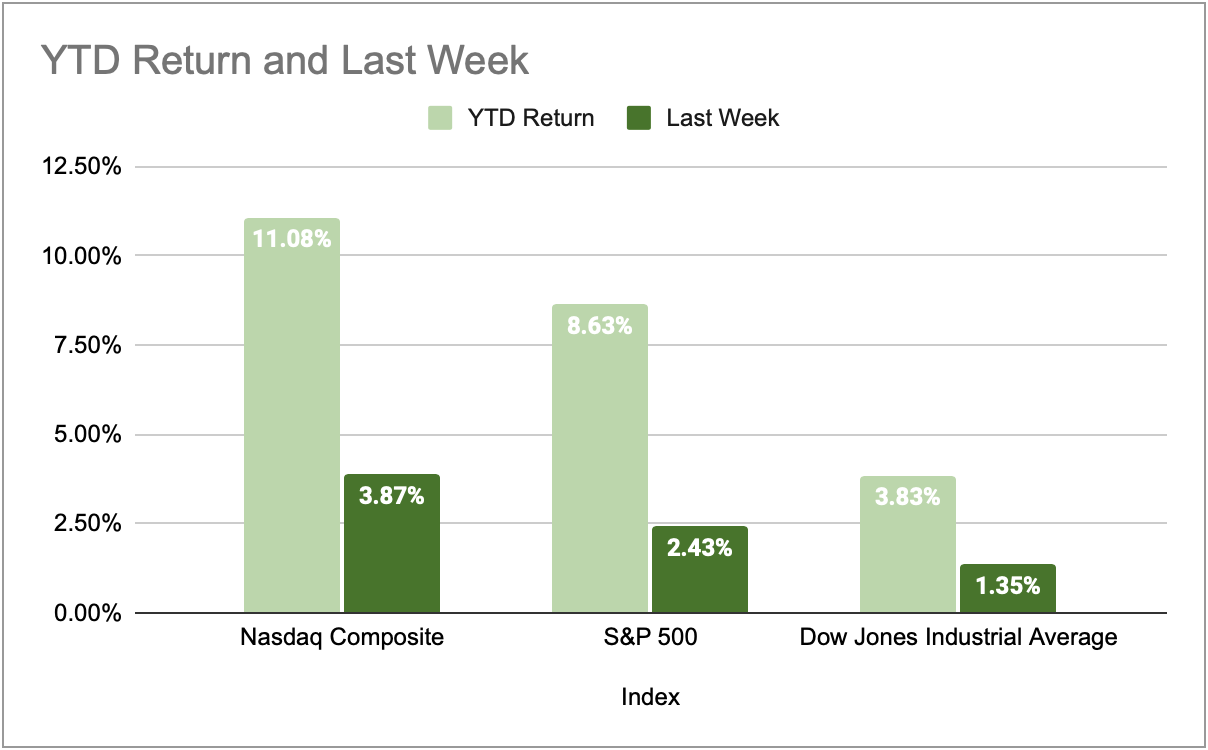

The major U.S. indices notched their third winning week in four. On Friday, the S&P 500 gained 0.8% while the Dow added 0.5% and the Nasdaq climbed 1%, leaving the tech‑heavy index at another record. For the week, the S&P 500 gained 2.4%, the Dow 1.3% and the Nasdaq a stunning 3.9%.

Investors shrugged off a soft July jobs report—nonfarm payrolls rose by only 73,000 and prior months were revised down by a combined 258,000—and focused instead on booming earnings and AI‑driven optimism. Treasury yields ticked higher as the Fed declined to hint at near‑term cuts, but that didn’t stop Apple and other mega‑caps from rallying.

The combination of a cooling labor market and strong corporate profits has the market in an odd Goldilocks mood: weak enough to make rate cuts plausible, yet strong enough to keep stocks levitating.

Mastery: As always, dips can be swift, so consider using rallies to rebalance rather than chase.

Earnings

They Can't Stop Winning

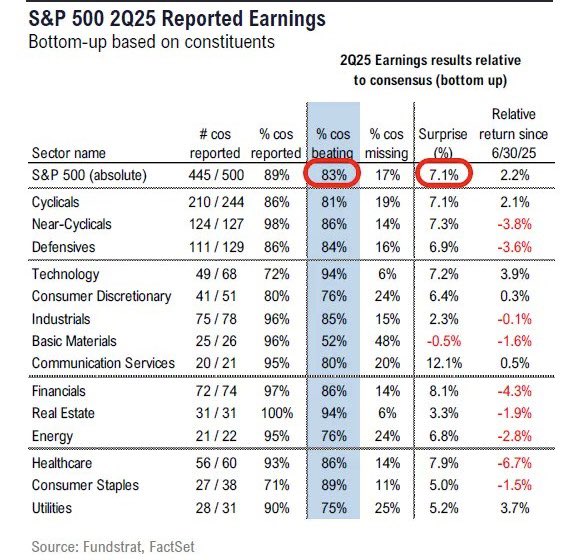

It’s not just a few tech darlings beating estimates—the entire earnings season looks like a broken drum machine. Out of the 453 S&P 500 companies reporting so far, 69% have beaten revenue expectations and 83% have beaten earnings estimates.

Growth in Earnings Per Share (EPS) is tracking 11.4% year‑over‑year while revenue is up 6.0%. AI‑adjacent firms like Palantir and Arista Networks gapped to fresh highs, but even industrial and healthcare names are joining the party. Palantir’s revenue surged 48% and it raised full‑year guidance. AMD’s sales jumped 32%, even though export‑control charges dented profits.

Disney’s diluted EPS nearly doubled, and Uber’s revenue beat forecasts with delivery and mobility growth of 25% and 19% respectively. Amgen posted a 9% revenue rise and a 21% gain in non‑GAAP EPS, while Novo Nordisk’s sales grew 18%.

It’s hard to find a miss—and that in itself may be the risk. When expectations reset higher, any stumble could be punished.

Mastery: Broad earnings strength justifies staying invested, but avoid loading up on whichever story stock is trending on social media. Remain diversified across sectors and remember that cycles always turn.

Economy

To Cut, or Not to Cut

On July 30 the Fed left rates at 4.25%–4.50% and Chair Jerome Powell refused to commit to a September cut, saying “no decisions” have been made and stressing the need to watch how tariffs affect inflation.

His data‑dependence pushed the probability of a September cut down to 46% from 65% the day before, according to CME’s FedWatch tool. Investors initially cooled their heels, but after the July jobs report and hefty downward revisions, Fed officials including Neel Kashkari and Mary Daly hinted that cuts could come “in the near term”.

Futures markets now price in a roughly 87% chance of a 25‑basis‑point cut—a reminder that markets swing from despair to euphoria faster than you can say “dot plot.” Powell’s reluctance means the central bank is not trying to rescue asset prices; it’s waiting for evidence that inflation is tamed.

Mastery: Interest rates have nothing to do with investment returns. Pay less attention to where rates are and focus on the economic data driving economic policy.

Responses