Good evening investors!

The Bureau of Labor Statistics released a new jobs report, and the numbers surprised many observers. Economists had expected U.S. employers to add around 110,000 jobs in July, but the report showed only 73,000 new positions. That’s a significant shortfall. Even more striking, the BLS revised its counts for May and June down by a combined 258,000 jobs, which economists noted is a much larger revision than usual because the agency received additional data and adjusted for seasonal patterns. These sharper-than-expected downward revisions suggest the job market may be losing momentum.

Not long after the report came out, President Trump fired the head of the BLS. He posted on social media that the numbers were fake and ordered her removal. Lawmakers from both parties spoke out against his decision. Former leaders of the BLS said firing her was “without merit” and that it would hurt trust in official statistics. When the person in charge of measuring the economy gets dismissed over bad news, it raises many questions.

So what does this mean for you? Slow job growth can point to a weaker economy, which can hurt company profits and stock prices. But a softer job market also makes it more likely that the Federal Reserve will cut interest rates. Lower rates often boost asset prices. The lesson: stay calm, stay diversified, and pay attention to how company earnings and consumer spending change over time. Is this the start of a bigger slowdown or just a small bump? We’ll find out soon, and I’ll keep you informed.

–Brian

In Today's Issue:

🥇 The bill comes due for stocks

🥈 Inflation is started to rise again

🥉 Big tech companies are dominating earnings

Markets

Tariff Turbulence

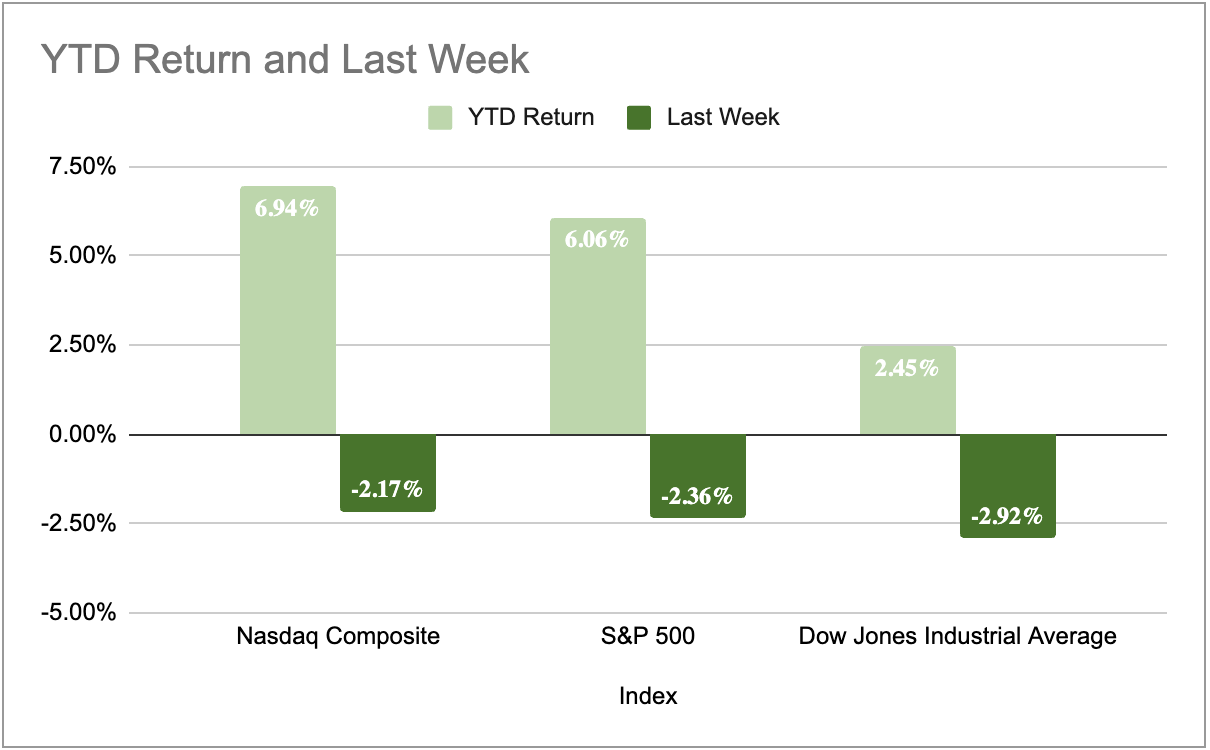

After six straight record‑setting closes earlier in the week, Wall Street got a wake‑up call on Friday. Fresh U.S. tariffs on dozens of trading partners and a surprisingly weak jobs report sparked the sharpest daily selloff in more than two months. The Dow slipped 1.23%, the S&P 500 dropped 1.6%, and the tech‑heavy Nasdaq tumbled 2.24%. For the week, the S&P 500 fell 2.36%, the Nasdaq lost 2.17%, and the Dow shed 2.92%. Wall Street’s fear gauge, the VIX, jumped to 20.38, its highest close since late June, and heavyweights like Amazon (down 8.3% after cloud results disappointed) and Apple (off 2.5% despite a strong revenue forecast) dragged consumer‑oriented stocks lower.

Zooming out, the picture remains surprisingly resilient. By late July, more than half of S&P 500 companies had reported second‑quarter results, and earnings growth is now estimated at about 9.8%, sharply above the 5.8% forecast at the start of the month. Roughly 81% of companies are beating analyst estimates, and the momentum behind artificial‑intelligence‑oriented tech firms continues to support the indexes. Despite last week’s setback, the S&P 500 is still up around 6% for the year. Valuations, however, remain elevated: the benchmark index trades at about 29.7 times earnings and offers a dividend yield near 1.24%, while the 10‑year Treasury yields roughly 4.23%. That keeps the risk‑reward balance in focus as tariffs, politics, and rate‑cut speculation drive volatility.

Are we headed for a deeper pullback or just a brief shake‑out? Investors will be watching earnings this week from Disney, McDonald’s, and Caterpillar, and listening for the Federal Reserve’s response to the soft jobs report, which sent rate‑cut odds soaring. Use this time to review your portfolio and ensure you’re comfortable with your exposure to cyclical sectors and high‑flying tech names.

Inflation

Guess Who's Back (It's Inflation)

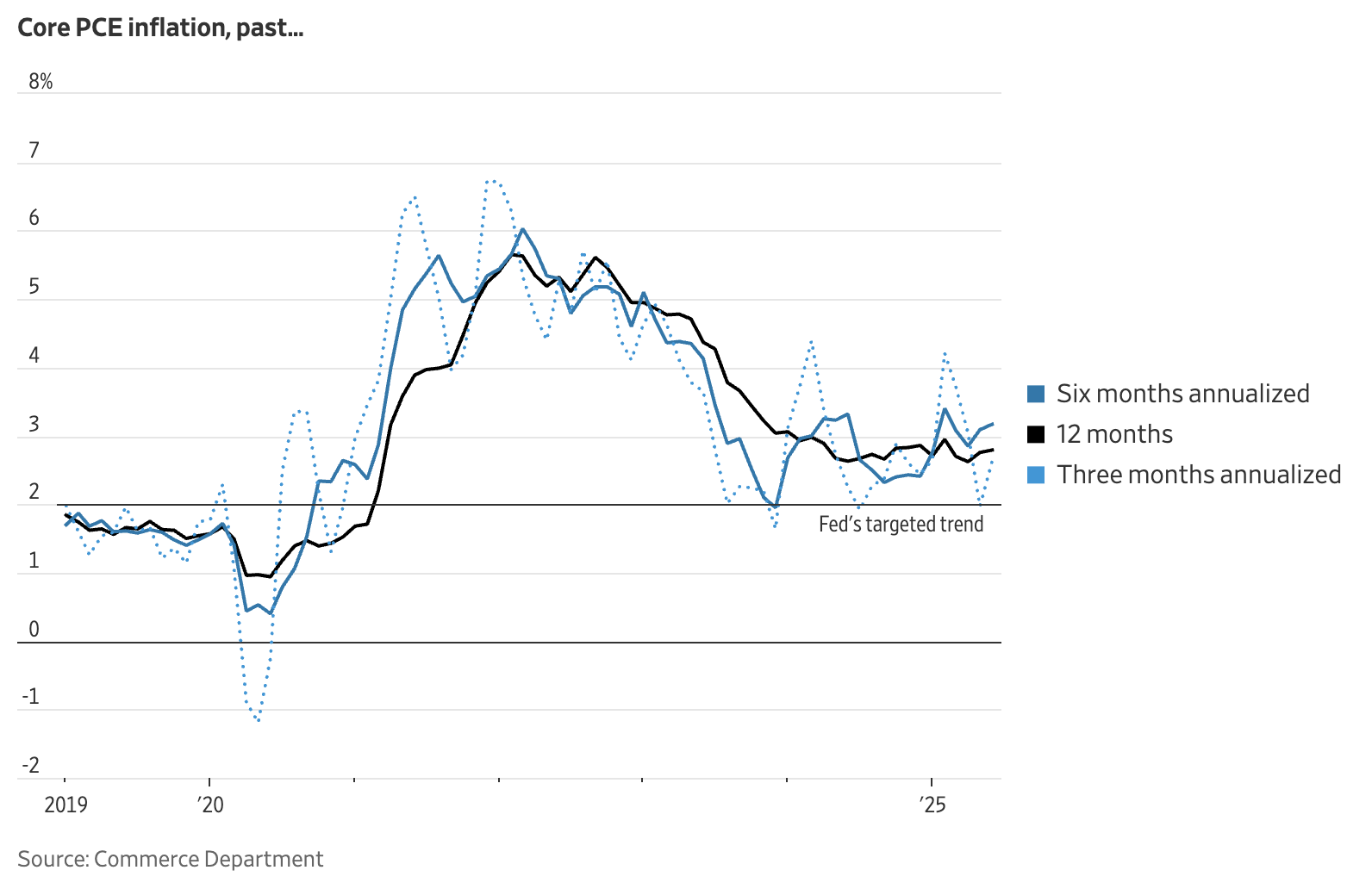

Last week’s personal consumption expenditures report showed that price pressures are picking up again. Overall inflation, as measured by the PCE price index, rose 0.3 % in June after a 0.2 % increase in May. Over the past year prices are up 2.6 %, compared with 2.4 % the month before. Core PCE, which strips out food and energy, also climbed 0.3 % in June and 2.8 % from a year earlier. Tariffs played a big role: the cost of furnishings and durable household equipment jumped 1.3 %, the largest rise since March 2022, while recreational goods and vehicles prices shot up 0.9 %. Clothing and footwear prices also moved higher. Even energy prices, which had been falling, rebounded by 0.9 %.

Consumers are still spending, but there are signs of strain. Spending grew 0.3 % in June after stalling in May, supported by a stable labour market and wage gains. The saving rate held at 4.5 %. Yet economists warn that renewed inflation and a cooling job market could curb purchases later this year. Fitch Ratings’ Olu Sonola noted that inflation is “diverging” from the Federal Reserve’s 2 % target and could delay rate cuts until at least October. Indeed, the Fed left its benchmark rate unchanged at 4.25–4.50 % last week and signalled caution. If tariffs continue to push up goods prices, the central bank may be forced to keep borrowing costs higher for longer, which can weigh on both consumer spending and stock valuations.

For investors, rising inflation is a two‑edged sword. Higher prices erode purchasing power, but they can also pressure the Fed to stay on the sidelines, keeping yields on cash and bonds relatively attractive. Watch how future PCE readings evolve; a sustained upswing could dampen the chances of a near‑term rate cut and increase volatility in rate‑sensitive sectors. On the flip side, if inflation cools again and consumer spending holds up, markets could regain their footing. Stay nimble and consider how persistent price pressures might affect different parts of your portfolio.

Earnings

AI Investment Hides Earnings Uncertainty

The latest earnings wave was dominated by the same familiar heavyweights. Microsoft smashed through a $4 trillion market cap, becoming only the second public company to do so. Its strong quarter was powered by booming cloud and AI demand; the company expects to spend a record $30 billion this quarter on data‑center investments, and its Copilot tools now boast over 100 million monthly users. Meta, meanwhile, continued its advertising resurgence—revenue jumped to $47.5 billion, well ahead of forecasts, and the company lifted the lower end of its annual capital‑spending plan to $66–$72 billion as CEO Mark Zuckerberg bets big on AI. Together, these AI‑focused giants now make up about a quarter of the S&P 500, underscoring how concentrated market leadership has become.

Elsewhere, results were more mixed. Amazon’s core e‑commerce and advertising businesses remained solid—ad revenue climbed 23%—but investors were rattled by thinner margins at its AWS cloud unit, where profitability slipped to 32.9%, the lowest since late 2023. The company’s sales outlook of $174–$179.5 billion for the current quarter edged past expectations, yet shares fell over 7% as CEO Andy Jassy signaled capital spending could reach around $118 billion this year. Apple offered a steadier counterpoint: its June‑quarter revenue climbed 10% to $94 billion, with double‑digit growth in iPhones, Macs and services, and it rewarded shareholders with a 26‑cent dividend. While the AI revolution continues to fuel outsized gains for some companies, these results suggest the spending race for dominance could pressure margins even as broader consumer demand holds up.

Responses