Good morning investors!

According to the Wall Street Journal, 45% of economists surveyed in April are predicting a recession this summer. At the same time, the Altanta Fed's real-time GDP tracker is estimating the economy to be growing at a healthy 3.8%. While all this is going on, the S&P 500 is up over 2% for the year (more on that below). So uh...are we having a recession or not?

The answer is likely that we are on the precipice of either a really strong or really bad economy, and it might even be both at the same time. And it's pretty unclear which one we are headed for. Here are the two major scenarios:

The Bull Case: While global trade is uncertain, the current administration will cycle out in a few years. Provided nothing catastrophic happens before then, we will come out the other side roughly the same as we went in. On top of this, AI is accelerating at an unprecedented pace and will drive growth and productivity gains in the workforce. GDP will increase, and everyone's lives will (on average) be better.

The Bear Case: We are currently in the "catastrophe," it's just more like a slow moving train of destabilization rather than a sudden jolt to the economy. Like in 2008, the economy is slowly deteriorating until suddenly it will all come crashing down. Companies will chase profits instead of growth, conducting mass layoffs to save money, and AI will simply make it easier to replace human labor, not enhance it. In an effort to "save" the economy, the government will deal the final blow by printing massive amounts of money, increasing the deficit further and triggering another wave of inflation. And this time, the average consumer won't be able to just "deal with it."

The Middle Case: There is nothing stopping both of the above outcomes to play out. Similar to the 2020 "K-shaped" economy in which the rich got richer and the less rich stayed less rich. In this scenario, the economy will be whiplashed by changing global relations, but big companies will have the resources to weather the storm, while smaller companies will get washed out. AI will lead to both productivity gains and output growth, but will also replace labor. And it will likely replace lower skilled and entry-level labor, which AI models excel at. While overall economic metrics like unemployment and GDP will look fairly healthy, digging deeper will show that some areas of the economic capture the majority of the gains, while others bear the majority of the losses.

Personally, I think we are headed towards either the middle case or the bear case. Check out my Recession Investing playlist on YouTube for full breakdowns on why I think the economy could be headed for a recession, and what you can do about it to safely grow your net worth. And I would love to hear from you, which of these outcomes sounds more plausible to you? Or is there a different one altogether that I'm not capturing here?

-Brian

In Today's Issue:

🥇 All Market Indexes are Green

🥈 May Jobs Report: "Good, Not Great"

🥉 The Corporate Profits Keep Profiting

Markets

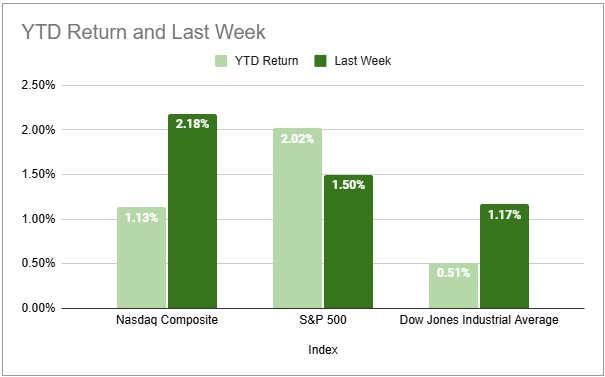

Everything is Green

Last week, the S&P 500 jumped 1.50%, while the tech-heavy Nasdaq shot up 2.18%, and the less volatile Dow Jones Industrial Average increased a more modest 1.17%. A swath of positive news drove markets higher, including somewhat easing trade tensions and progress of talks between China and the U.S. as well as a "good, not great" May jobs report.

Looking ahead, we are about a month away from the July 9 pause deadline on the "reciprocal tariffs" announced during Trump's so-called Liberation Day. And a month after that comes August 12 which is China's 90-day tariff extension while negotiations proceed. Both of these dates will be key points of potential market movement.

Nearer on the horizon we have a Fed meeting on June 18, where the options market is pricing in a zero percent chance of a rate cut. For those that follow the Fed, this comes as no surprise given Jerome Powell's remarks on holding steady until there is more certainty on Fiscal Policy. This will likely be the case for the July 30 meeting as well. If you were hoping that interest rates would come down anytime soon...it's gonna be a while.

Jobs

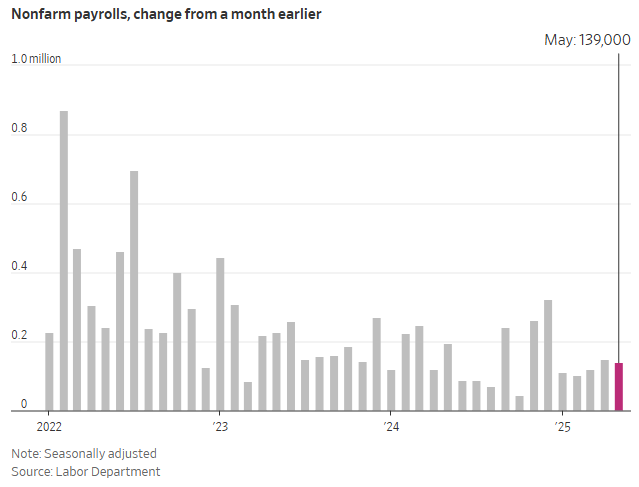

Companies Are Still Hiring

(source: WSJ)

In May 2025, U.S. job growth slowed to 139,000 new jobs, surpassing the anticipated 125,000 but signaling caution among employers amid ongoing tariff uncertainties. The unemployment rate remained steady at 4.2%, although underlying data indicated some weaknesses, including a significant drop in employment in the household survey. Despite this, stocks reacted positively, relieved the figures weren't worse, reflecting cautious optimism amid economic volatility.

Businesses continue to face difficulties planning and investing due to fluctuating tariffs and an aggressive immigration policy environment. Hiring practices are notably cautious, with fewer layoffs but also many positions left unfilled, reflecting uncertainty over future economic conditions. Temporary employment—typically an early indicator of economic stress—also fell, indicating that companies may be tightening their belts.

This update perfectly reflects the middle case scenario I outlined in the intro of this week's newsletter. The overall employment number is steady, but it's not the prettiest when you dig into the data. And let me know if you disagree, but everyone I talk to agrees that the job market is pretty tough right now. We could see these diverging trends develop further into a K-shaped economy.

Earnings

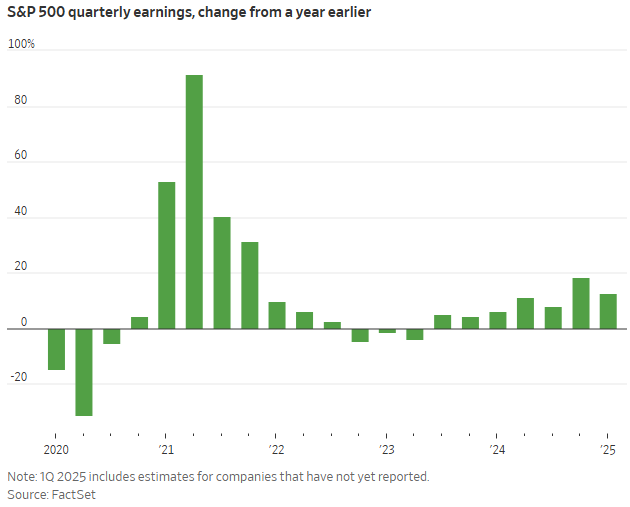

Corporate Profits Are Healthy

(source: WSJ)

Companies have been knocking it out of the park, with first-quarter profits for firms in the S&P 500 projected to rise by around 13% compared to last year, significantly surpassing analysts' initial expectations of about 7%. Companies like AutoZone, Nvidia, and Costco are in strong financial health, indicating a resilient corporate America despite ongoing economic uncertainty.

However, this positive earnings backdrop has been accompanied by caution among businesses due to escalating tariffs and unpredictable trade policy shifts. Tariffs were frequently cited during earnings calls, mentioned by 2,136 companies—more than any quarter since 2016—with firms including Delta Air Lines, Ford Motor, and Crocs even withdrawing financial guidance entirely due to uncertainties around future trade impacts. Walmart explicitly noted it would raise prices due to tariffs, illustrating direct consumer implications.

Looking forward, despite the solid recent earnings results, concerns persist around inflation and economic uncertainties, especially given projections from a University of Michigan survey indicating consumers expect prices to surge by 7.3% over the next year—the highest expectation since 1981. Businesses and investors remain watchful, balancing strong short-term corporate performance with caution due to continuing economic volatility.

Responses